How to Arrange Money Flow on an eCommerce Marketplace

The success of a marketplace greatly depends on how many sellers do business on the platform and how good they are. One of the most important attraction points for sellers is transparent and hassle-free marketplace transactions. It will be much easier for you to attract sellers to your platform if you offer them hassle-free transactions.

The thing is that transactions are in the core of your online marketplace: customers pay for orders → money goes to the marketplace sellers. This is the very basic operation that a marketplace can’t exist without. It looks simple but in real life, arranging cash flow among marketplace users can be a pain.

In this article, we talk about hidden rocks of the money flow arrangement on a marketplace, the ways you can organize transactions among customers and sellers, and the best options of money flow for different types of marketplaces.

What’s the payment routine on an online marketplace?

There are two general ways customers pay for orders on an online marketplace:

- Right on the marketplace with on-board payment methods: credit card, PayPal, Stripe, or any other popular payment method available on the marketplace.

- Outside of the marketplace: a customer pays the seller with a direct money transfer outside the platform: direct bank transfer, cash from hand to hand, cash on delivery, etc.

The first way is more common. Payments made through a third-party payment service right on the marketplace are secure and usually refundable. All the major marketplaces like Amazon work this way.

The second way is suitable for a marketplace of used items such as Craigslist. When buying on classifieds marketplaces, a customer usually meets the seller in person or interacts with them online outside of the platform to complete the transaction.

In this article, we’ll talk about the first way—when customers pay for orders via payment methods offered by the marketplace.

So, the scheme looks simple for a customer and a seller. The customer puts products to the marketplace shopping cart and pays via a credit card. The seller gets that money and ships the order. But what happens in between? Some supreme magic.

Three ways to make marketplace money flow transparent and hassle-free

One of the primary goals of an online marketplace is to facilitate the transactions among the marketplace users. You can achieve this by organizing the money flow the right way.

There are hundreds of proven third-party payment services that integrate with marketplaces. All of them are usually PCI-compliant and meet all the security requirements to process payments. The best option to avoid legal complications with accepting payments is to build your marketplace on a software platform that integrates with third-party popular payment gateways. For example, our marketplace platform CS-Cart Multi-Vendor integrates with over 70 payment services such as PayPal, Stripe, 2Checkout, Authorize.net, eWay, Sage Pay, and others.

All you’ll need to do to start accepting payments is to set up the payment gateway on the marketplace. All the third-party payment services are compliant with all the security standards, so that it will no longer be your headache.

Use a marketplace platform with built-in popular payment services.

Split, take, or move the whole amount to sellers?

There are three common methods of organizing money flow on an online marketplace:

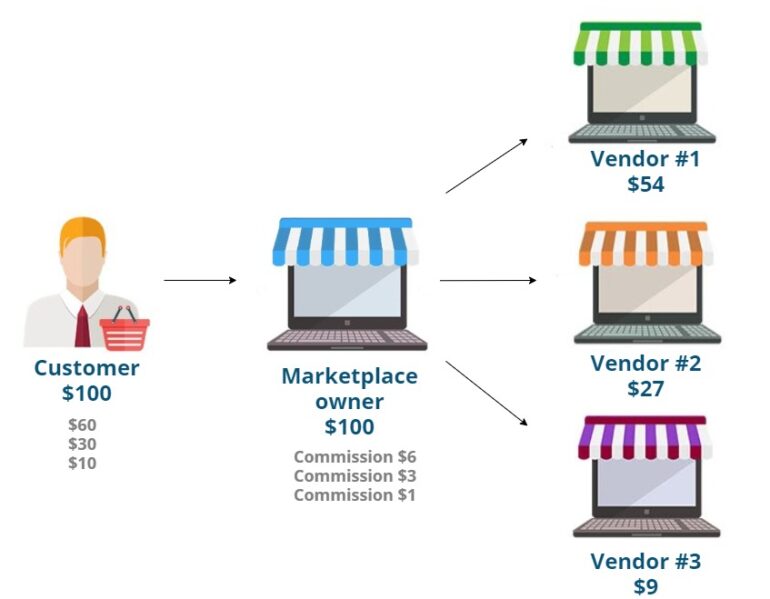

1. Customers’ money goes to the marketplace. The marketplace pays out to sellers their share regularly on a certain date.

Amazon works this way: the marketplace pays out to its professional sellers every 14 days via a bank transfer. It can take up to 5 days for the payment to appear on the seller’s account. Google Play also pays out to developers each month on the 15th for the previous month’s sales.

To ease the seller payout process, the marketplace software platform usually have these features:

- Vendor plans and commissions: you create vendor plans with certain conditions and set commissions.

- Accounting withdrawals: Based on the vendor plans, you automatically collect information about how much you owe to sellers and sellers can request withdrawals.

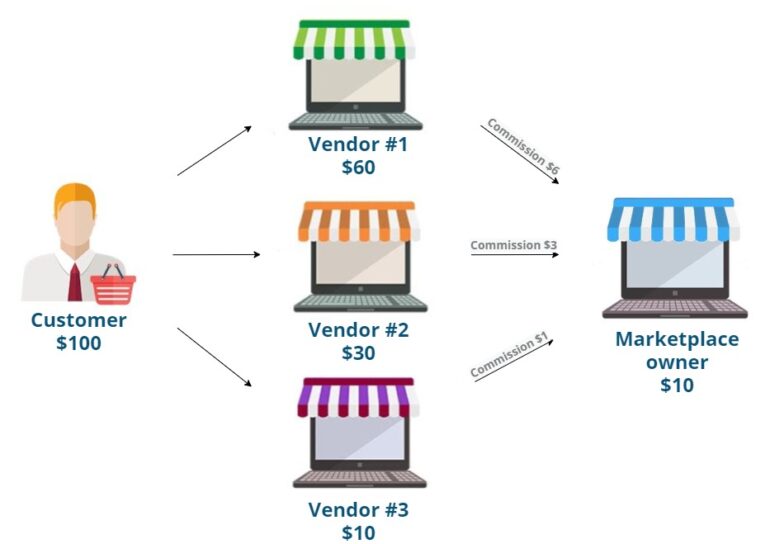

2. Customers’ money goes to sellers. Sellers pay out commissions for every order to the marketplace.

Etsy uses a similar money flow strategy. The money for every sale is deposited into the seller’s account the next business day after the sale is made. And sellers keep their balance positive to pay fees they owe to Etsy. What’s cool about this marketplace is that it created their own payment system called Etsy Payments, which is convenient for sellers and the marketplace.

For this method, marketplaces can use these features:

- Direct customer-to-vendor payments: customers pay directly to sellers, so that they receive all the money for orders.

- Vendor-to-admin payments: a seller pays out to the marketplace its part.

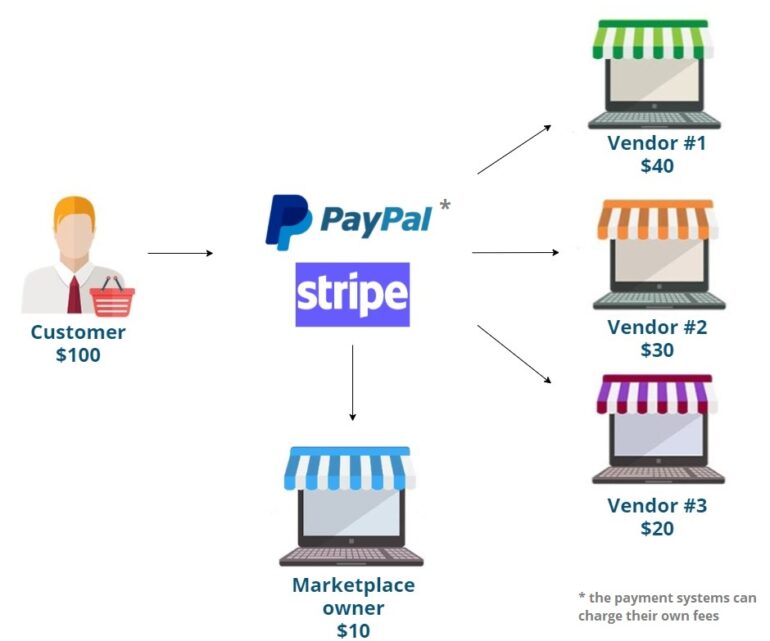

3. Customers’ money are split into two transactions automatically. The first transaction goes to the marketplace, the other—to sellers.

On Airbnb, a host gets paid within 24 hours after the guest check-in time. The marketplace automatically extracts its fees from the payout and transfers the rest of the money to the host’s account.

The money is split via payment systems such as:

- Stripe Connect

- PayPal Commerce Platform

From a regulatory perspective, getting all the money from customers and then paying out to sellers their share can be difficult. Authorities keep close tabs on such transactions to prevent money laundering through marketplaces.

To use the first method of organizing transaction flow (you receive the whole amount and pay your sellers), you’ll need to get to know your sellers closely: collect legal information, scan identity documents, collect personal and company information, names and addresses. And you will have to update this information regularly and keep up with the changing regulations.

What experts say

Elizabeth HicksCo-Founder of Parenting Nerd

I have faced a lot of trouble following local and international regulations when dealing with merchants of all kinds. I have had to stay updated with the rules and regulations every month as they tend to change more often due to Covid. Contacting every company and finding out about their policies has proved too hectic for me at times. Collecting and generating tax invoices has been another challenge that I have had to face throughout the year.

To avoid regulatory complications, you can split money from orders into two independent transactions or move the whole amount to sellers and take commissions from them after the transaction is complete.

Receiving all the money and sending sellers their part is not the best option if you don’t want to deal with legal and bureaucratic complications. It’s neither a good option for a marketplace with a large seller base—too much time needed to make manual payouts to all of them.

What are the pros and cons of the three money flow arrangement methods?

| Method | Pros | Cons |

|---|---|---|

| 1. All the money goes to the marketplace, then the marketplace transfers sellers their part. | + It’s easier for sellers start selling products + A customer pays just once + Hassle-free refunds | – A marketplace has to pay the money they owe to sellers and that’s difficult in terms of legal regulations – Sellers receive their money after a while |

| 2. All the money goes to sellers, then they pay a commission to the marketplace. | + A marketplace owner does not have to pay the money they owe to sellers + Sellers receive the money right after the payment | – A customer has to pay each seller separately, and they often can’t make just one payment – Each seller has to create their own payment methods. |

| 3. The money is split into two transactions automatically—one goes to the marketplace, the other goes to the seller. | + A customer pays once + Sellers receive the money shortly after the payment + A marketplace doesn’t have to split the money between seller | – Sellers need their own PayPal and/or Stripe accounts, and they must connect them to the marketplace – The payment systems can charge their own fees |

As you can see from the comparison table, the easiest option for both the marketplace and sellers is to split payments automatically via Stripe Connect or PayPal Commerce Platform.

Stripe could be a better option if you’re working with sellers who don’t have an eCommerce background. Stripe Connect Express Accounts greatly simplifies seller onboarding. Try their demo of fictional RocketRides marketplace.

The second easiest option is to move all the money to sellers and then charge them fees. Receiving the whole amount and paying out to sellers is convenient in terms of refunds but not the best options in terms of legal regulations.

What experts say

Richard Lubicky, founder of RealPeopleSearch, eCommerce expert

The most sustainable approach is when the eCommerce marketplace collects the payments from the customers and then settles the seller’s payments after a few days. This way, marketplaces can consider all the charges and deal with the customer product returns and replacements in a much better way.

Aviad Faruz, Chief Executive Officer at Faruzo

One of the many difficulties we’ve had with the first payment method (all money goes to the marketplace first) is that since it is a manual payment process, we have to overlook regulation compliance, chargebacks, and fraud prevention ourselves which is a time-consuming process. If we had gone with split payments, we wouldn’t have to do all of these ourselves and could have left it to the marketplace.

The most hassle-free money flow arrangement method is splitting payments into two transactions through Stripe or PayPal. Stripe is better in terms of seller onboarding.

Our marketplace platform CS-Cart Multi-Vendor supports all the three methods. Take a look at how you can arrange the money flow from the marketplace admin perspective.

What experts say

Anastasiya Kurganova, co-founder

of the kids products marketplace Oozor.ru

Within one year and a half after we started the marketplace, Oozor.ru was free for our sellers. They got a convenient platform to sell online, traffic, and orders without any fees. It was our conscious strategy. Firstly, we wanted to attract as many sellers as possible who would come to the platform for free with zero risks for their businesses. Secondly, in the beginning we didn’t really understand what monetization model would be the most efficient for us. This free period for sellers helped us understand how we could design the money flow.

In my opinion, commissions are the most fair money flow arrangement model. You sell—you pay. You don’t sell—you don’t pay. But for now, a big part of our sellers don’t accept payments online through payment gateways. And it’s a very important factor for a commission-based model with automatic payouts. The cause why the sellers don’t accept online payments lies in the shortage of technical knowledge and unsteadiness if micro-businesses. We actively motivate our sellers to start accepting online payments through PayPal and the number of connected sellers grows. For now, the number of sellers accepting online payments is still not enough to switch the marketplace to the commission-based model.

For now, we decided to use a monetization model based on vendor plans. Plans allow us get money from the sellers and at the same time this feature doesn’t depend on whether a sellers accept online payments or not.

Vendor plans have their ups and downs. The annual order value on our marketplace counts $700,000. We could get significant income from a commission-based model. This is a downside of our current monetization model. The others are ups: low-sale sellers pay 3% of their annual revenue for using a vendor plan. Top sellers pay 0.5%. This is way less than any possible commission. This model is beneficial for both us and our sellers. The absence of commissions motivate sellers to complete transactions on the marketplace and not outside of it to save money. It influences the traffic in the good way: sellers land their customers to Oozor.ru.

When 60% of sellers start to accept online payments, we will switch to the commission-based model cancelling vendor plans. We are looking into using payment services that split money automatically into two parts—for us and a seller. The more the process is automated, the more efficient it is. We are not planning to use any kind of manual payouts: we have a deep experience with manual payouts for services that were paid fully or partially and we realize how inconvenient it is. Especially when it comes to high volume of transactions. We are also looking into a hybrid model with annual vendor plans and commissions—a seller chooses the one that fits them best. Top-sellers might prefer vendor plans, low-volume sellers—commissions.

Money flow arrangement practices for product, service, and booking marketplaces

There are different types of marketplaces out there. You can group them in three categories:

- Marketplaces for products: electronics, apparel, used items, digital products, etc.

- Marketplace for services: home services, freelance jobs

- Marketplaces focused on booking: accommodation, cars

A thing they have in common is the transactions among customers and sellers. But the way the transactions are organized greatly depends on what these marketplaces sell.

How to arrange transactions on different types of marketplaces

Let’s say a marketplace offers cars for rent. A customer rents a car online for a specific date, and the marketplace withdraws the whole payment from the customer’s credit card. Then unexpected things happen: the customer’s trip is canceled, the customer changes the date of trip or even has to shorten or prolong the rent period, a car accident happens during the rent period.

All these events can cause the increase or decrease of the rent cost. If something of the above happens, the marketplace has to initiate a partial refund, take more money for more days of rent, or even charge the customer extra for covering the damage in case of an accident. Too much hassle. The best payment withdrawal option here was to freeze the amount on a credit cart and transfer the money to the marketplace account after the customer returns the car.

Here are some ideas on how and when to complete a transaction between a customer and seller:

| On marketplaces for physical products | 1. Initiate a transaction immediately: money from the customer’s credit card is transferred to the marketplace account immediately (within up to 72 hours). eBay works this way. 2. Preauthorize money on the customer’s credit card: best for global marketplaces and marketplaces for used items that need to be checked or tried on before buying. Aliexpress uses this method. 3. Negotiate price and complete a transaction outside of a marketplace: best for marketplaces for hand-made or used items, which price needs to be decided. Craigslist is a good example. |

| On marketplace for services | 1. Preauthorize money on the customer’s credit card: best for cases when the price for service is fixed and won’t change. Once the service is provided, the money is released to the provider (or not if you are not satisfied). 2. Negotiate price and complete a transaction outside of a marketplace: this one also works for service marketplaces—you meet with the service provider in person, negotiate the price and pay in cash or a bank transfer. 3. Provider invoices the customer in stages: suits for IT freelance jobs when a freelancer usually works on a big project and charges hourly. |

| On booking marketplaces | 1. Initiate a transaction immediately: when a customer books accommodation, the hotel gets money in hours (up to 72 hours). 2. Preauthorize money on the customer’s credit card: the customer’s bank guarantees that there is enough money on the credit card, and then transfers it to the seller within several days. 3. Negotiate price and initiate transaction immediately: some booking websites allow you to negotiate price with the seller and pay right on the platform. Airbnb uses all these methods. |

Handling refunds

Neither sellers, nor customers like product returns. But returns are a normal operation in a marketplace business workflow. The way you handle returns and refunds can influence your customers’ satisfaction.

Your sellers can issue full refunds or partial refunds. Full refunds are usually issued for a returned item. Partial—for damaged or incomplete orders.

On large marketplaces such as Amazon and eBay sellers initiate refunds themselves, which is the most common practice.

On eBay, if an item arrives damaged, doesn’t match the listing description, or if the buyer receives the wrong item, the seller must accept a return. Once the seller receives the item back, they use the built-in seller dashboard feature to issue a full or partial refund. The buyer receives the amount to the credit card.

On Amazon, returns are even easier. A customer requests a return in the account. The seller approves it. Then Amazon provides the customer with a prepaid UPS return label which allows him to return the item to any UPS drop-off point located across the US. Once the item comes back, the sellers issues a refund with a built-in RMA functionality in the seller’s dashboard.

This is a hassle-free return and refund method that saves the customer’s time and makes returns management easier for sellers. That’s why large marketplaces across the globe keep adopting this practice.

When it is better to distribute money on a marketplace manually

As we learned from the comparison we made earlier, the easiest method to arrange money flow on a marketplace is to automate it—split payments into two transactions through Stripe Connect or PayPal Commerce Platform. But there are a couple of situations where you would prefer manual payouts:

- You’ve just launched your marketplace. At the starting point, you usually test business processes, tweak them, play with functionality, and fine-tune the workflow. It is better to distribute money manually to avoid unforeseen bugs in automatic payouts, and as a result, dissatisfied sellers.

- You run a small or niche marketplace. If the transaction volumes are not that big on your marketplace, there’s no need to set up automatic payouts. You or your managers can process payments manually, saving on commissions taken by payment services used to split payments.

What experts say

James Khoury, an online retailer and CEO of Zendbox,

the intelligent eCommerce fulfillment solution driven by AI

Automation is the most efficient way if your aim is business growth. With so many aspects of e-commerce now being automated, why shouldn’t the marketplace payments be included?

The more automation involved at every step of the process, the more time retailers can spend on driving more customers and improving their product range.

As an online retailer and CEO of an e-fulfillment company I know that removing manual processes and allowing data to do the work can only be beneficial for marketplace sellers.

There may be the odd occasion where they see anomalies in the figures and then need to assess the information, but in most situations having an automatic split payment speeds up administration.

Summary

Organizing the money flow on your marketplace is a crucial part of building a successful multi-vendor eCommerce website. And one of the most challenging in terms of legal regulations. The more hassle-free and transparent the transactions are, the more sellers trust you and join your platform.

There are three methods of organizing a transparent transaction flow on an online marketplace:

- Customers’ money goes to the marketplace, then the marketplace pays out to sellers. This is the most complicated way to arrange transactions because of the legal regulations but the most convenient in terms of refunds and unexpected cash situations.

- Customers’ money goes to sellers, then the sellers pay out commissions to the marketplace. This is a convenient method for the marketplace because it doesn’t have to deal with legal and bureaucratic complications.

- Customers’ money split automatically: one transaction goes to the marketplace, the other—to the seller. This is the most hassle-free and convenient method for both the marketplace and sellers.

There are some cases where automatic payouts are not the best option. New-born marketplaces are in the stage of fine-tuning—to avoid unforeseen bugs, it’s not a good idea to use automatic payouts right off. Also, small marketplaces with low volume of transactions can pay out manually saving on payment systems’ commissions.

Depending on the marketplace type—product, service, or booking—the transaction processing can differ. Most of the marketplaces can use (and they do use) two ways of charging money: instant transaction or money preauthorization on the buyer’s credit card.

We’re on LinkedIn! Connect and learn more about our marketplace platform, company life, and all the updates.

Yan Anderson is the Head of Content Marketing at CS-Cart with over 10 years of experience in the eCommerce industry. He's passionate about explaining complicated things in simple terms. Yan has expertise in building, running and growing eCommerce marketplaces. He loves to educate people about best practices, new technologies, and trends in the global eCommerce industry.